Choosing the best bank for your small business is one of the most important financial decisions you will make. The right financial institution can simplify cash flow management, reduce fees, provide access to financing, and help position your company for growth. While there is no single bank that is perfect for every business, several national and regional institutions consistently stand out for their products, customer service, digital banking, and lending options.

This guide compares some of the best banks for small businesses, highlighting their strengths, weaknesses, and the types of businesses they serve best. It also explains why many growing companies combine traditional banking with accounts receivable factoring to maintain healthy cash flow.

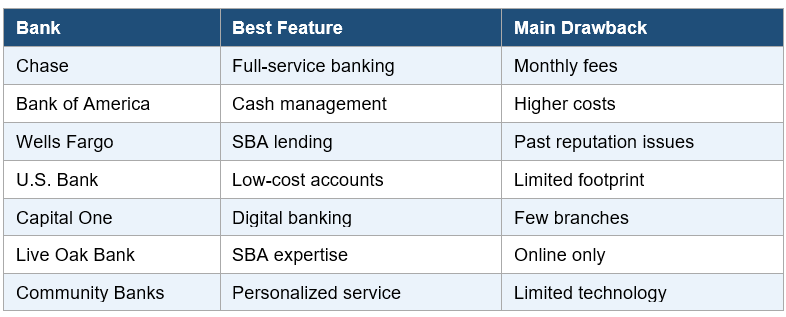

1. Chase Bank

Chase is one of the largest business banks in the United States and offers a wide range of checking accounts, merchant services, credit cards, and SBA lending.

Pros:

- Extensive branch and ATM network

- Strong online and mobile banking

- Excellent payment processing options

- Competitive business credit cards

- Wide variety of lending products

Cons:

- Monthly account fees unless balance requirements are met

- Higher wire transfer costs

- Smaller businesses may receive less personalized service

Best for: Businesses wanting a full-service national bank.

2. Bank of America

Bank of America offers scalable banking solutions from startups to established companies.

Pros:

- Strong cash management tools

- Excellent integration with accounting software

- Robust fraud protection

- Preferred Rewards for Business program

Cons:

- Fees can add up

- Some lending requirements are stricter than competitors

Best for: Growing businesses planning to expand.

3. Wells Fargo

Wells Fargo remains a major SBA lender and offers business banking nationwide.

Pros:

- Strong SBA lending history

- Wide branch availability

- Multiple checking options

- Good payroll integrations

Cons:

- Reputation challenges from prior regulatory issues

- Some products have higher fees

Best for: Companies seeking traditional business lending.

4. U.S. Bank

U.S. Bank is consistently recognized for business banking value.

Pros:

- Low-cost checking options

- Strong treasury management

- Good customer satisfaction

- Competitive merchant services

Cons:

- Limited branch footprint outside core markets

- Fewer specialty lending programs

Best for: Cost-conscious small businesses.

5. Capital One

Capital One combines modern digital banking with business banking products.

Pros:

- Excellent mobile banking

- No-fee business checking in many markets

- Strong customer experience

- Competitive credit cards

Cons:

- Limited branch locations

- Smaller business lending portfolio

Best for: Service businesses and entrepreneurs.

6. Live Oak Bank

Live Oak Bank specializes in SBA lending and operates primarily online.

Pros:

- Industry expertise

- Excellent SBA loan experience

- Competitive savings rates

- Nationwide availability

Cons:

- Limited in-person banking

- Primarily lending-focused

Best for: Businesses seeking SBA financing.

7. Local Community Banks and Credit Unions

Community financial institutions often provide personalized service that larger banks cannot match.

Pros:

- Local decision making

- Relationship-based lending

- Personalized customer service

- Competitive loan flexibility

Cons:

- Smaller technology budgets

- Limited branch networks

- Fewer specialized products

Best for: Businesses that value personal relationships.

Comparison Chart

How to Choose the Right Bank

Consider monthly fees, transaction limits, digital banking, lending availability, branch access, customer support, integrations with accounting software, and fraud protection. The best choice depends on your industry, transaction volume, and growth plans.

Banking Alone May Not Solve Cash Flow

Even excellent banks may not provide enough working capital for rapidly growing businesses because traditional loans often require lengthy underwriting and strong collateral. Businesses experiencing slow-paying customers often supplement traditional banking with accounts receivable factoring, which converts outstanding invoices into immediate working capital without taking on conventional debt.

Conclusion

The best banks for small businesses each offer unique advantages. Chase excels in full-service banking, Bank of America offers strong growth tools, Wells Fargo remains a leader in SBA lending, U.S. Bank provides excellent value, Capital One shines in digital banking, Live Oak specializes in SBA financing, and community banks deliver personalized relationships.

At American Receivable Corporation, we work alongside banks—not against them—to help businesses strengthen cash flow when traditional financing alone is not enough. Combining the right banking relationship with smart working-capital solutions can help your business invest confidently, meet payroll, and pursue new opportunities.

About American Receivable Corporation

Since 1979, American Receivable Corporation has helped businesses improve cash flow through accounts receivable factoring. We frequently partner with banks to provide flexible working-capital solutions that complement traditional banking relationships, allowing companies to grow without waiting for customers to pay outstanding invoices.