Business owners are constantly searching for ways to manage cash flow, fund growth, and navigate unexpected expenses. When working capital becomes tight, two common options often come to mind: invoice factoring and business credit cards. While both can provide access to funds, they serve very different purposes and can have dramatically different impacts on a company’s financial health.

Many business owners automatically reach for a credit card when cash flow gets tight. It is familiar, convenient, and readily available. However, relying too heavily on credit cards can create long-term financial challenges, especially for businesses that regularly wait 30, 60, or 90 days for customer payments.

Invoice factoring offers an alternative approach. Instead of borrowing money, businesses convert their outstanding invoices into immediate working capital. This distinction can significantly affect profitability, growth potential, and overall financial stability.

At American Receivable Corporation, we’ve spent decades helping businesses improve cash flow through invoice factoring. Understanding the differences between these two financing tools can help business owners make smarter decisions about how they fund operations and growth.

Understanding Business Credit Cards

Business credit cards provide a revolving line of credit that allows companies to make purchases and repay balances over time. They can be useful for short-term expenses, travel costs, office supplies, software subscriptions, and emergency purchases.

The appeal is obvious. Approval is often quick, funds are available immediately, and many cards offer rewards programs.

However, credit cards come with limitations. Credit limits may restrict access to larger amounts of capital, and interest rates can become expensive when balances are carried month after month.

For businesses facing recurring cash flow challenges caused by slow-paying customers, credit cards often treat the symptom rather than solving the underlying problem.

What Is Invoice Factoring?

The process is straightforward:

- Deliver products or services.

- Send an invoice to the customer.

- Submit the invoice to the factor.

- Receive an advance on the invoice value.

- Customer pays according to agreed terms.

- Remaining funds are released after fees.

Unlike credit cards, invoice factoring does not create additional debt. It simply accelerates access to money already earned.

The Fundamental Difference

The biggest distinction between invoice factoring and credit cards is simple.

Credit cards borrow against the future.

Invoice factoring unlocks money already owed to your business.

This difference becomes increasingly important as businesses grow.

Cash Flow Challenges for Growing Businesses

Ironically, growth often creates cash flow pressure.

A staffing company may land a large contract but need payroll funding before receiving payment. A manufacturer may need raw materials to fulfill orders. A trucking company may need fuel and driver payroll weeks before customer invoices are paid.

Many business owners bridge these gaps using credit cards.

The problem is that customer payment delays frequently outlast the credit card billing cycle, creating interest charges and growing balances.

Invoice factoring aligns funding directly with sales activity, creating a more scalable cash flow solution.

Comparing Costs

At first glance, credit cards may appear less expensive.

Many cards advertise introductory rates or rewards programs. However, businesses that carry balances often face double-digit interest rates that can accumulate rapidly.

Invoice factoring costs are generally transparent and tied to invoice volume.

The key question isn’t simply which option has a lower fee. Business owners should ask which solution creates greater opportunities.

If invoice factoring allows a company to accept larger contracts, take supplier discounts, or avoid payroll disruptions, the return on investment may far exceed the cost.

Scalability Matters

Credit cards typically have fixed limits.

A company with a $25,000 credit limit still has a $25,000 credit limit whether sales are $100,000 or $1 million.

Invoice factoring works differently.

As sales increase and receivables grow, available funding often grows as well.

This scalability makes invoice factoring particularly attractive for businesses experiencing rapid growth.

Impact on Balance Sheets

Business credit cards increase liabilities and debt obligations.

High credit card utilization can also impact business credit profiles and borrowing capacity.

Invoice factoring generally improves liquidity without creating traditional debt.

For companies focused on maintaining healthy financial statements, this distinction can be valuable.

When Credit Cards Make Sense

Credit cards still play an important role in many businesses.

They can be effective for:

- Small recurring purchases

- Travel expenses

- Emergency expenditures

- Building business credit

- Taking advantage of short-term rewards programs

Used responsibly and paid off quickly, credit cards can be useful financial tools.

The challenge arises when they become the primary source of working capital.

When Invoice Factoring Makes Sense

Invoice factoring is often ideal when businesses:

- Invoice other businesses

- Offer payment terms

- Need working capital quickly

- Are experiencing rapid growth

- Have payroll-intensive operations

- Want to avoid additional debt

Industries such as staffing, transportation, manufacturing, construction, wholesale distribution, and oilfield services frequently benefit from factoring solutions.

A Real-World Example

Imagine a staffing company that places workers for a large customer.

The company invoices $100,000 but won’t receive payment for 60 days.

Option 1: Use Credit Cards to Cover Payroll

Interest accumulates while waiting for payment.

Option 2: Use Invoice Factoring

Receive funding shortly after invoicing and cover payroll without increasing debt.

The second approach often creates a more predictable and sustainable cash flow cycle.

Why More Businesses Are Choosing Invoice Factoring

Today’s business environment demands flexibility.

Rising costs, labor shortages, supply chain disruptions, and economic uncertainty make consistent cash flow more important than ever.

Business owners increasingly recognize that financing growth with credit cards can become expensive and restrictive.

Why American Receivable Corporation?

Since 1979, American Receivable Corporation has helped businesses convert receivables into reliable working capital.

As an owner-managed factoring company, ARC focuses on relationships, responsiveness, and customized funding solutions. We understand that every business has unique needs, and we work closely with clients to create programs that support growth.

Whether you’re a startup seeking stability or an established company pursuing expansion, invoice factoring can provide the liquidity needed to move forward with confidence.

The Bottom Line

The debate between invoice factoring and credit cards is not about determining a universal winner. Both tools serve important purposes.

Credit cards can be excellent for convenience and short-term purchases.

Invoice factoring is often the stronger solution for businesses that need ongoing working capital, scalable funding, and improved cash flow without taking on additional debt.

Invoice factoring helps businesses access cash faster, support growth, and focus on opportunities rather than Invoice Factoring vs. Credit Cards:waiting for payments.

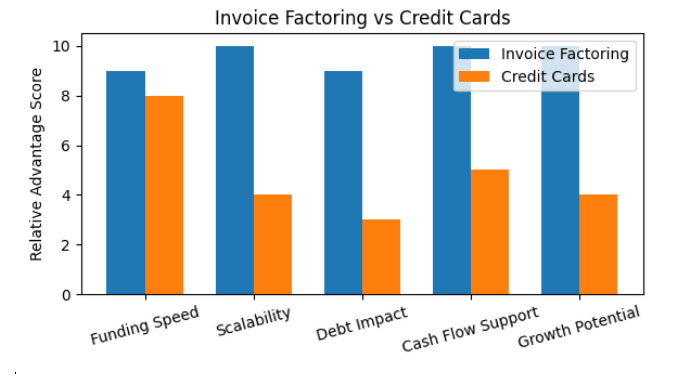

Comparison Chart: Invoice Factoring vs Credit Cards