When businesses need working capital to manage cash flow, fuel growth, or cover payroll, two popular financing options often come up: asset-based lending and factoring. While both provide access to capital using business assets, they function very differently. Understanding asset-based lending vs. factoring is essential for choosing the right solution for your company’s cash flow needs.

This guide breaks down how each option works, their key differences, and which type of business benefits most from each approach.

What Is Asset-Based Lending?

Asset-based lending (ABL) is a type of loan secured by business assets such as accounts receivable, inventory, equipment, or real estate. A lender establishes a borrowing base and advances a percentage of the value of those assets. The borrower then repays the loan over time with interest.

Asset-based lending is commonly used by established companies with strong financial controls, predictable cash flow, and the ability to meet reporting requirements. These loans often come with covenants, audits, and ongoing compliance obligations.

What Is Factoring?

Factoring involves selling accounts receivable to a factoring company in exchange for immediate cash. Instead of waiting 30 to 90 days for customers to pay invoices, businesses receive an advance—often within 24 hours. The factoring company then collects payment directly from the customer.

Unlike asset-based lending, factoring is not a loan. There is no debt added to the balance sheet, and approval is primarily based on the creditworthiness of your customers rather than your business credit.

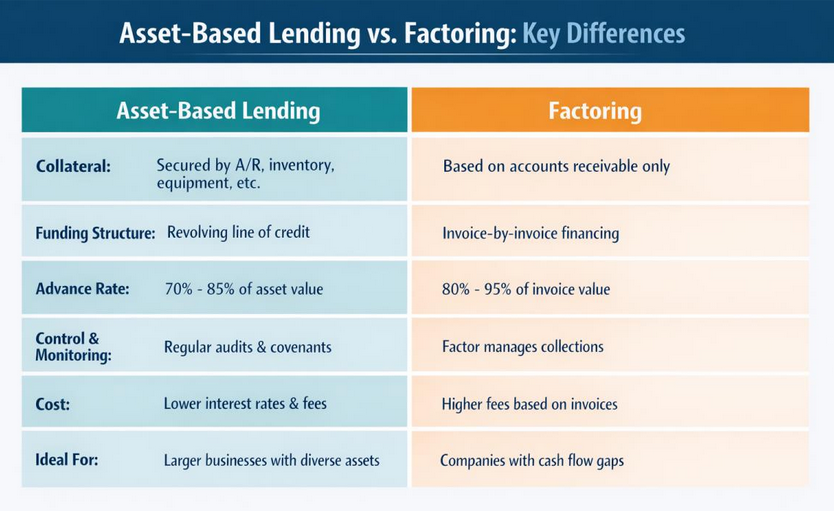

Key Differences Between Asset-Based Lending and Factoring

Although both solutions leverage receivables, the structure, risk, and accessibility are very different. The chart below highlights the main differences between asset-based lending vs. factoring.

Which Option Is Better for Cash Flow?

From a cash flow perspective, factoring offers immediate and predictable access to working capital. As soon as invoices are generated, businesses can unlock cash without waiting for customer payments. This makes factoring especially valuable for companies experiencing rapid growth or tight payroll cycles.

Asset-based lending can provide lower long-term costs, but it lacks the speed and flexibility many businesses need. Delays in approval, borrowing base calculations, and covenant compliance can limit access to funds when timing matters most.

Why Factoring Often Wins for Small and Mid-Sized Businesses

For many small and mid-sized companies, factoring is the more practical solution. It requires less paperwork, no long-term debt commitment, and scales naturally as sales increase. Businesses do not need perfect credit or years of operating history to qualify.

Factoring is also ideal for industries such as staffing, transportation, construction, manufacturing, and oilfield services, where long payment terms are common and payroll or vendor costs must be met quickly.

When Asset-Based Lending Makes Sense

Asset-based lending can be a good option for mature businesses with strong balance sheets, internal accounting teams, and consistent revenue. Companies seeking a traditional lending relationship and lower interest costs may prefer this route, provided they can meet the strict requirements.

However, for businesses that need speed, flexibility, and simplicity, asset-based lending may feel restrictive.

When comparing asset-based lending vs. factoring, the right choice depends on your business size, growth stage, and cash flow urgency. Asset-based lending offers structure and long-term financing, while factoring delivers speed, flexibility, and immediate cash access.